Asian family offices are navigating one of the most complex investment environments in recent memory. On one hand, tokenised alternatives, digital assets, and private markets offer compelling return opportunities beyond traditional equities and fixed income. On the other, managing wealth across multiple jurisdictions introduces a layered web of tax obligations, regulatory requirements, and compliance demands. Singapore family offices that succeed in 2025 are those that balance innovation with governance.

Quick Summary

The most forward-looking Singapore family offices are expanding into tokenised real estate, private credit, and digital asset funds while simultaneously investing in the governance infrastructure to manage cross-border complexity. Philanthropy in family offices is also rising as a strategic tool: it provides tax efficiency, legacy alignment, and a mechanism for next-generation engagement.

Top picks for balanced alternative investment strategies:

- Best overall: Multi-asset SFO with dedicated alternatives committee and tax advisory retainer

- Best for tokenised assets: Licensed digital asset fund via MAS-regulated manager

- Best for philanthropy integration: Donor-advised fund with annual grant-making process

- Best for cross-border compliance: External tax counsel engaged across each operating jurisdiction

“Tokenised private credit and real assets are no longer experimental for family offices; they are becoming a standard allocation in the alternatives bucket.” (MAS FinTech Festival Panel, November 2024)

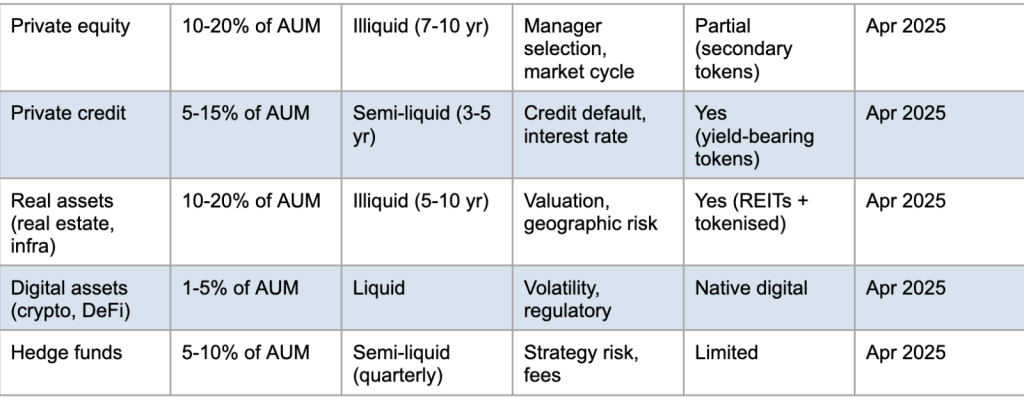

Comparison Table (Last updated: April 2026)

How to Choose Your Alternatives Strategy

The decision framework for alternatives begins with liquidity tolerance. Family offices with near-term capital requirements (within three years) should limit illiquid allocations to no more than 20-30% of total AUM. Families with longer horizons and stable operating business cash flows can afford higher illiquid allocations of 40% or more.

For tokenised alternatives specifically, MAS has established clear guidelines under its Payment Services Act and Securities and Futures Act frameworks. As of Q1 2025, tokenised securities must be issued by a MAS-licensed entity. Families should only access tokenised products through regulated platforms.

Philanthropy in family offices is increasingly woven into the alternative strategy as a distinct allocation. Philanthropic capital deployed through impact vehicles or donor-advised funds can serve multiple purposes: tax efficiency under Singapore’s Income Tax Act, legacy alignment, and next-generation engagement. Families that integrate philanthropy into their investment policy statement report higher family cohesion scores and lower succession conflict rates, according to a 2024 Mercer study.

Cross-border tax management requires proactive engagement with tax counsel in each jurisdiction. Common triggers for cross-border tax obligations include: management and control tests for corporate entities, permanent establishment rules for investment activities, and controlled foreign corporation (CFC) regulations applicable to Singapore entities holding assets in jurisdictions such as India, the UK, or the US.

Q: How are Asian family offices balancing traditional wealth preservation with new investment opportunities in private markets and alternative assets?

The tension between traditional wealth preservation and new alternative opportunities is one of the defining strategic challenges for Asian family offices today. Families built on conservative capital preservation instincts, often anchored in fixed income, property, and blue-chip equities, are being pulled toward private markets and tokenised assets by the promise of higher returns and greater diversification.

The most effective resolution is a barbell strategy: a core preservation portfolio (50-60% of AUM) anchored in investment-grade bonds, dividend equities, and liquid real assets, alongside an opportunistic portfolio (20-30% of AUM) targeting private equity, private credit, and alternatives. The remaining allocation covers cash and near-liquid instruments for operational needs and tactical opportunities.

Philanthropy in family offices sits within this framework as a distinct third allocation, typically 5-10% of AUM, deployed through donor-advised funds or direct impact investments. This three-bucket approach, documented in Mercer’s 2024 Asia Family Office Survey, allows families to honour their preservation instincts while capturing the return premium available in private markets, without the governance confusion that arises when all allocations are managed under a single mandate.

The 6 Best Practices for Managing Tokenised Alternatives and Cross-Border Risk

1. Access Tokenised Private Credit Through MAS-Regulated Platforms

Best for: Family offices seeking yield enhancement with partial liquidity

Quick Facts

- Global tokenised private credit market exceeded USD 8 billion in Q1 2025 (RWA.xyz, 2025) | MAS Project Guardian has tokenised over USD 1 billion in institutional financial assets | Yields on tokenised private credit range from 8-14% per annum (as of Q1 2025)

Pros

- Lower minimum investment sizes compared to traditional private credit funds

- Secondary market trading potential reduces lock-up risk

- Transparent on-chain performance data

Trade-offs

- Regulatory framework is still evolving | Smart contract risk and custodian risk require due diligence

Source: MAS Project Guardian; RWA.xyz Market Report Q1 2025

Last verified: April 2026

2. Integrate Philanthropy as a Strategic Allocation

Best for: Families seeking tax efficiency, legacy alignment, and next-gen engagement

Quick Facts

- Singapore’s Community Foundation and National Volunteer and Philanthropy Centre (NVPC) administer donor-advised fund structures | Tax deduction of 250% available for qualifying donations to Institutions of Public Character (IPC) in Singapore (IRAS, 2025) | Philanthropy in family offices in Asia grew by 31% between 2021 and 2024 (Asia Philanthropy Circle)

Pros

- Significant tax efficiency for qualifying donations

- Builds family legacy beyond financial wealth

- Engages next-generation family members in stewardship

Trade-offs

- Grant-making requires governance and due diligence process | Returns are non-financial

Source: Inland Revenue Authority of Singapore (IRAS), 2025; Asia Philanthropy Circle 2024

Last verified: April 2026

3. Establish a Cross-Border Tax Management Framework

Best for: Family offices operating across two or more tax jurisdictions

Quick Facts

- OECD Pillar Two minimum tax rules apply to multinational family office groups with global revenues above EUR 750 million (OECD, 2024) | Singapore has 100+ double tax agreements as of 2025 (IRAS) | Common cross-border issues: substance requirements, transfer pricing, CFC rules

Pros

- Reduces double-taxation risk

- Enables tax-efficient profit repatriation

- Supports compliance across all operating jurisdictions

Trade-offs

- Requires ongoing external tax counsel investment | Rule changes require policy updates

Q: How are Asian family offices navigating cross-border tax, regulatory, and compliance challenges across multiple jurisdictions?

Cross-border complexity is the single most cited operational challenge among Asian family offices managing wealth in two or more jurisdictions. The core issues are layered: each country of investment, incorporation, and beneficial ownership may impose its own reporting obligations, tax treatment, and regulatory requirements.

Leading impact investing family office practitioners address this through three disciplines. First, they maintain a live jurisdiction matrix: a document, reviewed quarterly with external tax counsel, that maps each entity and asset against its relevant regulatory and tax obligations. Second, they appoint a compliance lead within the family office, separate from the investment team, whose sole responsibility is regulatory calendar management. Third, they select domicile and holding structures deliberately, choosing Singapore partly because its extensive DTA network (100+ agreements) reduces the risk of double taxation across the family’s operating geographies.

MAS’s AML/CFT requirements, OECD Pillar Two minimum tax rules (for larger groups), and FATCA/CRS reporting obligations are the three frameworks that generate the most compliance workload for Singapore-based family offices in 2025. Families that invest in robust compliance infrastructure early consistently avoid the far greater cost, both financial and reputational, of regulatory violations.

Source: OECD Pillar Two Framework; IRAS Singapore DTA Network 2025

Last verified: April 2026

4. Develop an Impact Investing Framework

Best for: Families seeking financial returns alongside measurable social or environmental outcomes

Quick Facts

- Impact investing family office allocations in Asia grew from 9% to 16% of AUM between 2021 and 2024 (GIIN, 2024) | Singapore’s MAS Sustainable Finance Action Plan provides a regulatory roadmap | GIIN reports median impact investment returns of 10-12% net IRR for private equity impact funds

Pros

- Aligns investment with family values

- Access to growing pool of institutional co-investors

- Meets ESG reporting requirements in multiple jurisdictions

Trade-offs

- Impact measurement frameworks require specialist resources | Deal flow for verified impact opportunities is limited

Source: Global Impact Investing Network (GIIN) Annual Survey 2024

Last verified: April 2026

5. Allocate to Tokenised Real Estate for Diversification

Best for: Families seeking real estate exposure without single-property concentration

Quick Facts

- Global tokenised real estate market projected to reach USD 1.4 trillion by 2030 (BCG, 2024) | Singapore REITs (S-REITs) offer an established listed entry point; total S-REIT market cap: SGD 100+ billion (SGX, 2025) | Minimum tokenised real estate investment: USD 5,000-50,000 on regulated platforms

Pros

- Fractional ownership reduces minimum capital commitment

- Geographic diversification across asset types

- Transparent on-chain rent distribution

Trade-offs

- Regulatory treatment of tokenised real estate varies by jurisdiction | Liquidity in secondary markets remains thin

Source: Boston Consulting Group Digital Assets Report 2024; SGX 2025

Last verified: April 2026

6. Engage a Compliance and Regulatory Affairs Adviser

Best for: Family offices operating across Asia with multiple regulatory touch points

Quick Facts

- MAS Notices and Guidelines on Anti-Money Laundering (AML) require annual compliance reviews for registered entities | Cross-border investment activity may trigger reporting obligations in each jurisdiction | Regulatory violations carry penalties of up to SGD 1 million for AML breaches (MAS, 2024)

Pros

- Proactive identification of regulatory risks before they materialise

- Supports MAS examination readiness

- Reduces personal liability for family office principals

Trade-offs

- Ongoing advisory retainer cost: SGD 50,000-200,000 per annum | Can slow deal execution if not well-integrated

Source: Monetary Authority of Singapore AML/CFT Guidelines 2024

Last verified: April 2026

Best for Specific Use Cases

Best for Tokenised Asset Exposure

MAS-regulated tokenised private credit platform with yield-bearing tokens and secondary market access.

Best for Philanthropy and Tax Efficiency

Donor-advised fund through Singapore Community Foundation, targeting IPC-qualified recipients for 250% tax deduction.

Best for Cross-Border Compliance

External tax counsel engaged across Singapore, India, and key offshore jurisdictions, with annual compliance calendar.

Best for Impact Investing

MAS-aligned impact mandate with GIIN-certified measurement framework and quarterly impact reporting.

Best for Real Asset Diversification

Blended S-REIT listed allocation with selective tokenised real estate exposure for geographic diversification.

FAQs

Are tokenised digital assets regulated in Singapore?

Yes. Digital payment tokens and tokenised securities are regulated under Singapore’s Payment Services Act (PSA) and Securities and Futures Act (SFA) respectively, administered by MAS. Entities offering tokenised investment products must hold the appropriate MAS licence. Investors should verify the regulatory status of any platform before committing capital. (Source: MAS, April 2026)

What tax benefits are available for philanthropy through a Singapore family office?

Qualifying donations to Institutions of Public Character (IPCs) in Singapore attract a 250% tax deduction under the Singapore Income Tax Act. The deduction applies to cash donations and certain gifts-in-kind. Families should consult a Singapore-qualified tax adviser to confirm eligibility, as conditions apply and the framework is subject to change.

How do Singapore family offices manage OECD Pillar Two obligations?

Singapore enacted its Qualifying Domestic Minimum Top-up Tax (QDMTT) legislation in 2025, effective for financial years beginning on or after 1 January 2025. Family office groups with global revenues below EUR 750 million are generally not in scope, but should confirm their position with a qualified tax adviser. (Source: IRAS, 2025)

How can DBS help family offices navigate alternatives and cross-border complexity?

DBS Private Banking provides access to a curated selection of alternative investment opportunities, including private credit, private equity, and real assets, through its Alternatives platform. The bank’s private banking advisors work alongside external tax and legal specialists to support family offices managing multi-jurisdiction complexity. Learn more at the DBS Asian Family Office page.

Learn more about DBS Private Banking family office services at https://www.dbs.com/private-banking/wealth-planning/the-asian-family-office.page

WE SAID THIS: Don’t Miss…UAE–Saudi Economic Ties Get a Major Boost with New Trade Bridge